- Uswitch.com>

- Mortgage comparison>

- Best First-Time Buyer Mortgage UK 2024

First-time buyer mortgages

Taking out your first mortgage can be daunting...

Let our expert broker partner Mojo help find you the best deal for your circumstances and guide you through the process

How to get a first-time buyer mortgage with Uswitch and Mojo

Mojo Mortgages is an award-winning mortgage broker. Their experts can compare deals to find the best first-time buyer mortgage for you.

Add your details

Provide your details so Mojo Mortgages can find first-time buyer mortgage deals that are suited to you and your circumstances

Compare deals with a recommendation

Your Mojo expert will compare the best first-time buyer mortgage deals and call you to recommend those suited to you

Get your mortgage

Your Mojo expert will help you secure your first-time buyer mortgage deal.

Mojo Mortgages can compare first-time buyer mortgage rates from over 70 lenders across the whole of the market

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

What is a first-time buyer mortgage?

A first-time buyer mortgage is not a specific type of product - although some lenders tailor certain mortgages towards first-time buyers. Generally, though, first-time buyers have access to the same mortgage deals as any other buyer.

You’re classed as a first-time buyer if you:

Have never owned of part-owned a home before, anywhere in the world

You won’t be classed as a first-time buyer if you:

Have ever owned or part owned a home anywhere in the world

Have inherited or had a home bought for you, even if you've now sold it

You’re buying jointly with someone who has previously owned a property

How much can I borrow as a first-time buyer?

Most lenders base loan size on a multiple of your annual income, typically between four to four-and-a-half times what you earn. The fact that you're buying for the first time won't usually make a difference.

Lenders also look at your affordability, however, which is not quite as straightforward as your income. They'll need to weigh your income against any debts and regular expenses you have.

Our calculator can give you an idea of what you might be able to borrow based on your income and deposit - although a mortgage broker can give a more accurate estimate based on your actual full circumstances allowing you to compare first-time buyer mortgages

How much deposit do I need for a first-time buyer mortgage?

You'll need a deposit worth at least 5% of the value of the property you want to buy for a 95% loan-to-value (LTV) mortgage. This is the lowest deposit most lenders will accept, unless you look at a specialist mortgage.

The more deposit you can provide, the better the rates available to you typically are, so even offering 10% deposit, rather than 5% can have an impact.

The actual monetary value of your deposit depends on the price of the home you want. This table demonstrates how much deposit you would need per LTV, in order to buy the average first-time buyer home* in the UK.

*Average property value taken from Zoopla March 2024

| Average first-time buyer property value March 2024 | Deposit percentage | Actual deposit needed |

|---|---|---|

| £244,100 | 5% | £12,205 |

| £244,100 | 10% | £24,410 |

| £244,100 | 15% | £36,615 |

| £244,100 | 20% | £48,820 |

Different types of mortgages for first-time buyers

Your individual circumstances, such as financial stability and mortgage preferences, will always determine which is the 'best mortgage' for you. Remember, a whole of market mortgage broker can help you review all of the options available to you, and sometimes has access to offers you won't find yourself.

You could consider:

Fixed-rate mortgage

The interest rate is 'locked in' for a specific period on a fixed-rate mortgage deal. Typically, the initial interest rate is higher than on a variable rate deal, but you’re protected from external factors, such as rising interest rates.

The downside is that you won’t benefit if rates fall. When a fixed-rate mortgages deal ends, you’re moved onto the lender’s standard variable rate (SVR) unless you choose to remortgage.

Standard variable rate mortgage

SVR rates are set at the lender’s discretion, so they're able to change them at any time. Once your initial deal has finished, you'll move onto your lender's SVR automatically.

This rate is normally higher than the other deals available on the market, as it's the lender's default rate of interest. However, SVRs don’t have any penalties to move mortgages or overpay, so some people choose to stay on them, depending on what they plan to do next.

Latest UK remortgage statistics show the SVR in May 2023 stood at 7.44% (compared to 5.71% for the average two-year fixed rate 95% LTV mortgage).

Tracker rate mortgage

Tracker mortgages follow an external financial indicator, most often the Bank of England (BoE) base rate. They’re usually set at a certain percentage above that rate, so every time the indicator rises or falls, the interest you pay changes by the same amount.

Tracker deals tend to start out cheaper than fixed-rate mortgage deals, but if rates rise, they can get expensive. If rates fall, your interest should fall too, so you’ll pay less each month.

Discount-rate mortgage

Discount rate mortgages are set at a certain percentage below your lender’s SVR for the duration of the deal. Your mortgage interest and repayments will therefore change when the SVR does.

Other factors that may affect your interest rate include a rise in the lender’s cost of borrowing, regulation and internal targets. As they are not directly linked to any external factors, they are a little harder to predict than trackers.

Capped and collared mortgages

Some variable-rate mortgages (trackers and discounts) come with caps (or ceilings), which means that the amount you pay each month will never rise above a certain level.

Collars (or floors) are far more commonly seen, however, and this is where the provider sets a minimum amount that your interest rate can never fall below. If possible, it's best to avoid deals with collars, as they can minimise any savings you would make with a variable rate.

Offset mortgage

Offset mortgages use your savings to reduce the amount of interest you pay each month. If you have substantial savings, they are kept in linked account(s), and lenders deduct the value of them from your mortgage balance before charging interest.

Some providers also allow family offset mortgages, where a family member can use their savings to reduce the amount of interest you pay.

Government schemes available to first-time buyers

It can be difficult to save a deposit for your first home in the current financial climate, but there are a range of government schemes available those first-time buyers without access to help from family or friends that would be needed to make use of guarantor or family-assisted mortgage:

Shared ownership

A shared-ownership mortgage lets you buy between 10% and 75% of a property and pay an affordable rent on the remaining share - so you can get on the property ladder with a smaller deposit and more affordable repayments.

You can usually gradually increase your ownership to 100% through a process known as “staircasing”.

First homes scheme

The first homes scheme is attached to specific new-build homes, and allows first-time buyers and key workers earning below £80,000 (£90,000 in London), to purchase them for 30-50% less than their market value.

Each council has different eligibility conditions, but key workers or those with work or family connections to the area are likely to be prioritised.

Right to Buy/Right to Acquire

The right to buy and right to acquire schemes allow local authority (council) and housing association tenants respectively, to buy their homes at a discount on the market value.

Typically you'll need to have lived in a council or housing association property for a minimum of three years in total, although not necessarily consecutively. The discount available will related to the length of time you've been a tenant.

How to apply for a mortgage as a first-time buyer

When to apply

The best time to apply for a mortgage:

When you’ve got yourself into a stable financial position

When your credit file is in good standing

When you've saved a decent amount of deposit

Before you go to application stage:

Determine how much you can borrow - a mortgage agreement in principle (also known as a mortgage in principle or decision in principle details how much the lender is likely to lend you. Many estate agents won’t allow prospective buyers to view properties without one

Find a house you love

Make an offer

Once accepted, submit your formal mortgage application for the amount you've offered the seller

What documents do I need?

The lender will want to see evidence of the property you're buying, your income and your identity. It's worth preparing the following documents in advance of meeting your mortgage broker:

Proof of identity - such as a passport or driving licence

Proof of current address - utility bills or bank statements can be used for this

Proof of income - This is typically three to six months of payslips if you’re employed and 12-36 months of accounts and tax calculations if you’re self-employed

Three to six months of bank statements - the lender will use these to check on your spending habits to make sure you will be comfortable managing repayment

You can find more detail in our article: What do I need to apply for a mortgage?

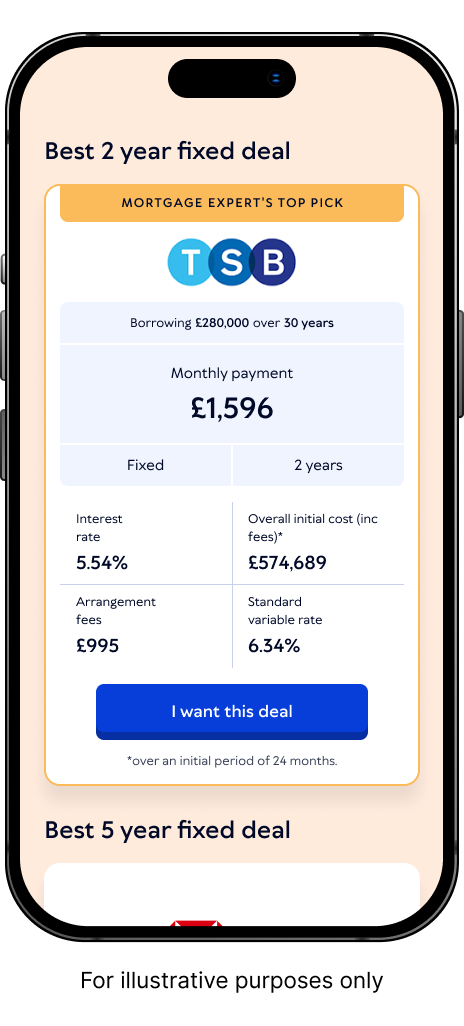

First-time buyer mortgage rates

Approaching your first mortgage can be daunting, so it's often a good idea to speak to an experienced broker, like our partner's at Mojo mortgages. They can provide you with invaluable guidance and a first-time buyer mortgage comparison when you're choosing the most suitable mortgage to buy your first home with.

Most people tend to be looking for the best first-time buyer mortgage rates available, and this is certainly something that a whole of market broker can help you find. However, to qualify for the best mortgage rates available, it's a good idea to:

Save as a large of a deposit as possible - this will reduce the LTV (loan to value) of your borrowing, giving you access to more competitive deals

Boost your credit score - as well as potentially giving you access to a higher loan, boosting your credit score will also make you less risky to lenders, meaning they can offer you a more competitive deal

What else to consider when getting a mortgage for my first home

Current financial status in the UK

Mortgage rates can change quickly, so the deals available to you when you get an agreement in principle are quite different by the time you actually submit your application, especially if it's taken you a long time to find the right home.

It's a good idea to stay up to date with current mortgage rates throughout the home buying process.

Flexibility on property requirements

It’s important to understand that very few first-time buyers are able to get exactly what they want in their first home. It's common to have to compromise on at least one element, such as considering a more affordable area or a smaller home than you initially planned.

When considering location, remember to think about the things that will affect your future life in the property the most, whether that’s proximity to transport, distance from family members or being nearby excellent schools.

Your budget

It’s important to be fully aware of and budget for the full costs of home ownership, rather than just your mortgage repayments. It’s also worth noting that your initial repayment could be slightly higher due to interest charged from the date that you moved in, if applicable.

Home insurance, average utility bills and council tax can all be researched prior to selecting a home, to help you not to take on more than you can manage. We've also compiled a list of the fees involved with the home buying process:

Mortgage arrangement fees - sometimes referred to as a product fee

Legal costs - including conveyancing and land search fees

Home insurance - most lenders will insist that you have buildings insurance as a part of the mortgage terms and conditions. Contents insurance is not required, but it is recommended

Property survey - this pays the lender's fee to ensure that your chosen property is worth the value that you've offered

Stamp duty - In England and Northern Ireland you won’t pay any on your first home, so long as it costs below £425,000, Different stamp duty rules and terminology apply in Scotland (LBTT) and Wales (LBT) - See the FAQs for more details.

Buying your first home is exciting but can also be stressful! Speak to a mortgage expert beforehand for support and guidance that eases the burden.”Kellie Steed, Mortgage Content Writer

First-time buyer FAQs

What is a mortgage in principle?

A mortgage in principle, often called an agreement or decision in principle, indicates how much a mortgage provider might be willing to lend you based on your financial situation. This document can be helpful when you start looking for a property, as they let estate agents and sellers know you’re a serious buyer.

It doesn’t guarantee a lender will give you a mortgage but it provides an indication of whether you’ll be accepted and for what amount. It’s also not binding, so you’re able to change your mind, should you not want to go ahead with the full mortgage application after taking a mortgage in principle.

If you struggle to get an agreement in principle, you’ve got time to address any problems, rather than coming unstuck later on in the mortgage application process.

What is a guarantor mortgage?

This is when a family member or close friend offers to guarantee your mortgage, often using their own property or savings as collateral. They are promising to step in and pay your mortgage if you can’t make the repayments yourself.

It is an arrangement that helps reassure lenders that you’re a safe bet for a loan, but there are risks involved for the guarantor.

What is shared ownership?

Shared-ownership lets you buy a percentage of a property with a commercial partner, such as a housing association, owning the rest.

The scheme allows you to purchase between 10% and 75% of the property value and pay rent on the remainder. You can usually gradually increase your ownership to 100%, although be sure to check the terms and conditions.

How do joint mortgages work?

A joint mortgage is where you buy a home with someone else, for instance, a partner, friend or family member. Typically a joint mortgage is between two people, but it’s possible to buy jointly with up to three other people (four in total) with some lenders.

Pooling resources means that you should be able to raise a larger deposit, and the mortgage offer will be based on your combined income. If this helps increase your LTV, you should also get better rates. Depending on the type of mortgage used, you’ll typically own the property jointly with the other applicants.

How does Stamp Duty work for first-time buyers?

As a first-time buyer in England and Wales, you’re eligible for a Stamp Duty discount. If the property is worth £425,000, you pay no Stamp Duty Land Tax (SDLT) at all.

If the house costs between £425,001 and £625,000, you pay SDLT at 5% on anything over the £425,000 threshold.

If the house costs more than £625,000, you don’t benefit from the discount.

The rules in Scotland are different, but first-time buyers can still get a discount, with the zero-tax threshold at £175,000.

Welsh first-time buyers do not benefit from a Land Transaction Tax (LTT) exemption, but you won't pay any LTT on properties under £225,000.

It's important to note that if you're buying with someone else who has previously owned a property, this will forfeit your first-time buyer status.

Should I buy freehold or leasehold for my first home?

Most buyers tend to favour freehold, as this means that you own the property and the land it sits on. Most, but not all houses are freehold. However, the majority of flats and apartments are leasehold. With a leasehold property you own the property but lease the land that it’s built on.

In some cases it can be beneficial to have a leasehold property, as it means that you won’t be responsible for maintenance of the external parts of the property, or the buildings insurance. There are pros and cons involved with both types of ownership - read more about freehold vs leasehold properties.

Should I get a longer term mortgage

Many buyers remortgaging during the cost of living crisis are considering extending their mortgages to make the monthly repayments more affordable, by spreading them out over a longer period of time.

Whether or not this is the right option for you will depend on your circumstances, particularly your current age and finances. However, it’s important to understand that extending the term of your mortgage means that you will pay more interest overall. Working with a whole of market mortgage broker to compare the best first-time mortgage rates can be helpful to best understand your current position.

What loan to value is best for first time buyers?

The lower the loan to value ratio of your borrowing, the better. This will both increase your choice of lender/deal and the competitiveness of the interest rates available to you.

It’s not always easy to save a large amount of money for a deposit in today’s economy however, and there is no one size fits all mortgage. A broker will be able to discuss this with you, conduct a first-time buyer mortgage comparison and make recommendations based on your individual circumstances.

What is the best mortgage for first time buyers?

There's not really one product that will suit all first-time buyers, as it will come down to your individual circumstances and your home ownership preferences. This can be a tricky decision to make and there is an overwhelming number of deals and information to sift through, so it can be very helpful to speak to a mortgage broker to compare the best first-time buyer mortgage deals for you.

First-time buyer mortgage guides

There are lots of factors to consider when taking out your first mortgage, this helpful range of guides may help...

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions. Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website. Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH. Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215) Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH, and head office is WeWork No. 1 Spinningfields, Quay Street, Manchester, M3 3JE. To contact Mojo by phone, please call 0333 123 0012.