- Uswitch.com>

- Mortgage guides>

- Remortgage To Release Equity 2024

Remortgaging to release equity

If you’ve built up equity in your home, you could release the cash by increasing your mortgage. We look at how releasing equity from your home works.

Release equity from your home

Responsible Life can help you find the right equity release options for you and your circumstances

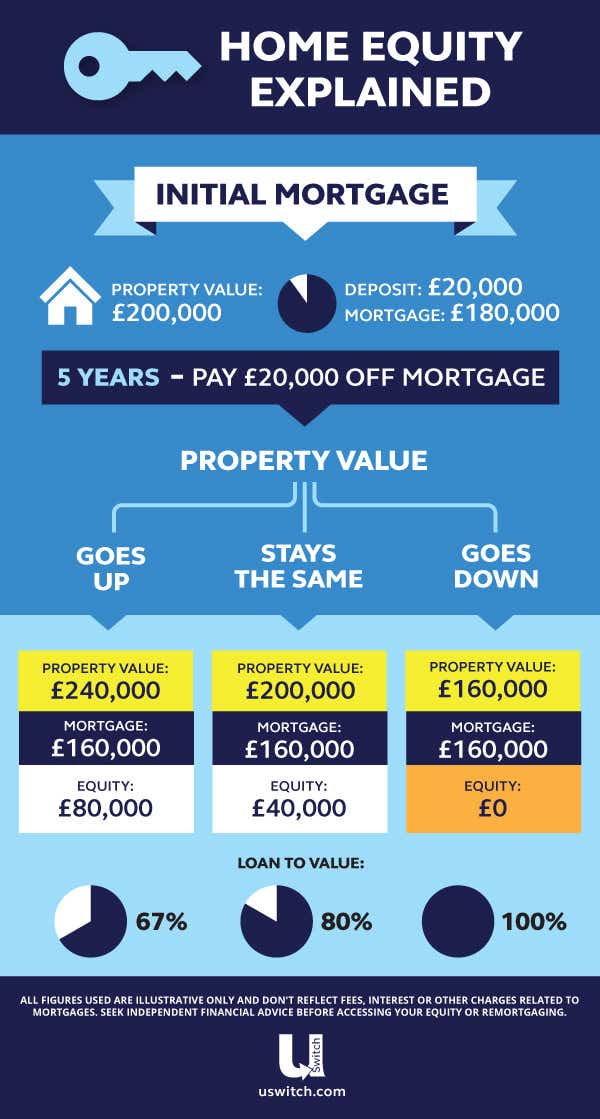

What is equity and how do I know how much I have?

Equity is the value of your home you don't pay any mortgage on, including the deposit you originally put in when you bought it. This means putting a larger deposit down puts you in a better position from the beginning of your mortgage deal.

There are two ways that the proportion of your home that you own (or your equity) can increase:

As you reduce your mortgage debt with monthly repayments, the amount you still owe reduces, and therefore as time goes on, you are borrowing a lower and lower percentage of the total value of your home (unless this falls due to a shrink in the housing market). But this is not the case for an interest-only mortgage, as the debt does not reduce through your monthly payments.

The value of your home increases. This will have the same impact as repaying some of the loan in terms of your level of mortgage equity (although you will still owe the same amount) as it will reduce the loan-to-value (LTV) of your borrowing (LTV is how much you borrow compared to the value of your home).

In most cases you will benefit from a combination of both of the above. You can work out how much equity you have by subtracting your remaining mortgage debt from the actual value of your home.

For example:

The value of your home was £350,000 when you first bought it. You put in a deposit of £35,000 and took out a mortgage of £315,000. You have made mortgage repayments worth £20,000 so your equity is currently £55,000. This leaves a remainder of £295,000 left to pay on your mortgage.

If the house price has also increased by £10,000, the equity would now stand at £65,000.

Don’t forget that house values do fluctuate and, if you’ve had your home valued by your mortgage lender for borrowing purposes, the value might not be quite as high as estimates from property websites.

Why might I need to use equity in my home for borrowing?

It's not uncommon for homeowners to borrow more money from their mortgage lender (or with a new one) secured against the equity in their homes. This is known as remortgaging to release equity.

This is possible because the equity serves as a deposit for the increased borrowing. Bear in mind, however, that increasing your borrowing will automatically increase the LTV of your borrowing, which may mean that you don’t qualify for such competitive mortgage rates.

Many people remortgage for a cash lump sum, which is often used to pay for home improvements that can add value to your home, to pay for their children’s education or to help a family member afford their first home, but it can usually be used for any legal purpose. Some people find it a good way to consolidate debts, as mortgage interest rates can be lower than typical loan interest rates.

This won’t always be the cheapest way to borrow more money, however, especially with current mortgage rates not being as competitive as they have been in recent years. It’s also important to remember that a mortgage term is typically longer than the average personal loan, meaning you will pay more interest overall.

How to access your equity

The most obvious way to access your equity is by selling your home. Typically, your equity would be put towards a deposit to buy a new home but you could keep back some of the money to use for other purposes.

Don’t forget that if you do sell your home you will have buying and selling costs as well as solicitor’s fees and removal costs to pay as well as the extra cost of taking on a bigger mortgage if you’re holding on to some of the equity. Make sure you weigh the pros and cons before taking this step.

Can I use the equity in my house as a deposit?

Yes, if your equity has increased, you can use it as a deposit, or maybe even buy a home outright if you have enough.

If you 'downsize' and move into a lower value home, you can turn your equity into cash if there is some left over once you’ve bought your new home.

How to remortgage to release equity from your home

If you don't want to move home, you can remortgage to borrow against the equity in your home simply by switching to a new mortgage with a new lender or through a new deal with your existing lender (known as a product transfer).

When you remortgage to release equity you take out a new mortgage deal that is larger than your existing one, using equity as a deposit.

For example: If you owed £100,000 on your existing mortgage, but took out a new mortgage of £120,000, you would be left with £20,000 extra, although there could be various fees to pay that would eat into that (an arrangement fee to take out the new mortgage for instance).

By remortgaging for a higher value you would have 'sold' £20,000 of your equity, as you would now only own £80,000 of the £200,000 value of your home, rather than £100,000.

It’s best to wait until your current mortgage deal has ended before remortgaging to release equity as you usually have to pay early repayment charges (ERCs) to switch mortgage before this point. However, you may still be able to borrow more from your existing lender as a separate loan.

Compare remortgages

Whether you're looking to save money with a remortgage or borrow more, comparing deals with the help of an expert broker can help you get the best deal for your circumstances.

How much equity can I release?

In theory, you can release as much as will take you up to the maximum LTV allowed, although lenders have to make sure you can afford to pay back the loan before agreeing to the increase.

If you’re releasing the equity for home improvements, the value it will add to your home could offset or even surpass the extra interest you would pay.

How the loan to value affects your borrowing

According to UK remortgage statistics, Mortgage lenders typically base loan size on a maximum LTV that they are willing to lend, typically between 75-85% when remortgaging to release equity. So this would be the maximum percentage of the value of your home that they will allow you to borrow once the additional borrowing is added to your original loan.

Mortgage interest rates are also based on the LTV of your borrowing, with a lower LTV typically leading to lower interest rates. This means that if you extend your loan too much, you may minimise the benefit that your equity will have on your interest rates.

What will happen to my mortgage repayments?

Of course, if you increase your borrowing, your repayments will also go up. Also the higher the LTV, the higher the interest rates you’re likely to be offered, so don’t be tempted to release more equity than you need to. You’ll also end up paying more in interest over the life of the loan.

Some of this additional cost may be offset if your new mortgage deal has a lower interest rate – either because you have a lower LTV due to increased equity, or if interest rates fall generally due to changes in the market.

You could also increase the length of your mortgage term to minimise the increase, but you’ll be paying even more interest overall because you’ll be borrowing the money for longer.

Things to consider before remortgaging for cash

Before you consider getting a larger mortgage, you need to weigh up the cost of remortgaging against the value of your equity.

Equity amount - work out the value of your home when you bought it minus how much of your mortgage you still owe. Your lender will be able to tell you how much you would have to pay to redeem your mortgage (including any ERCs if your initial deal hasn’t ended). It’s also a good idea to get a current valuation of your home to see if it has increased in value. You can get an idea of how much your house is worth by checking the Land Registry for similar property sales in your local area. You won’t necessarily be able to increase your LTV to the same as it was originally, as it's still about what you can afford to pay back

Assess risk adequately - if you’re hoping that further increase in the value of your property will balance out the increase in borrowing, bear in mind that just because property prices have gone up in the past, it doesn't mean they will continue to do so

Don’t overstretch yourself - have a serious think about the long term mortgage affordability, including the overall increase in interest you’ll pay over the entire mortgage term, as well as the larger monthly repayments. Remember to include any ERCs that apply if you’re planning to leave your current deal early

Compare mortgage rates - mortgage interest rates rise and fall fairly often, and sometimes the changes can be more dramatic than others, like the huge rises seen in 2022. Timing can be key to snatching up the right deal for you, so stay up to date with the market and always seek professional advice from a mortgage broker if you want greater certainty about your decision

Pros and cons of remortgaging to release equity

As with any form of borrowing, there are benefits and drawbacks to releasing equity, although exactly how these will apply to you will depend on your personal circumstances. They could include:

Pros

You can make good use of the money held in your home (or equity) that you wouldn’t otherwise be able to access without selling your home

The cash can be used for almost any legal purpose

You can typically borrow a larger amount than personal loans are able to lend

So long as you don’t borrow the full value of the equity in your home, the additional borrowing shouldn’t change your LTV (and therefore mortgage interest rates) too much

Cons

Your monthly repayments will most likely be higher

You will pay more interest on your mortgage overall due to the added borrowing

You will typically pay more mortgage interest than you would on a personal loan, due to the length of the term compared to relatively short personal loan terms - this means that it could be more expensive, even if the interest rate is lower

It will be easier to slip into negative equity (where you owe more than the value of your home) if house prices fall, as you will have reduced the equity you originally held

If you borrow more than your increase in equity the LTV will rise meaning you can’t access such competitive mortgage interest rates

Alternative options for releasing equity

If your personal circumstances, high early repayment/arrangement fees or low equity growth mean that remortgaging doesn't seem like a sensible option at the moment, there are a few other ways you can borrow money if you need to.

Further advance from your existing lender

Sometimes your mortgage provider may be able to offer a further advance on your existing mortgage. This will avoid any costs involved in getting a new remortgage deal, such as early repayment charges and new product fees.

Personal loan

A personal, or unsecured, loan will enable you to borrow amounts up to £50,000 over a period of between one and 10 years depending on the lender.

If you can afford to pay back the money within a year or two, a personal loan could work out cheaper than borrowing the money by remortgaging, but you may face some large monthly repayments.

As a personal loan is unsecured lending, you will need a good to excellent credit rating to borrow at headline rates.

Credit card

A credit card is a much more flexible way to borrow smaller sums up to about £5,000, although credit limits vary according to personal circumstances.

However, credit cards are not an economical way to borrow cash, as you will pay extra fees and interest on any withdrawals. Unlike loans and mortgages, however, you can adjust the size of your repayments each month, provided you meet the minimum repayments.

A low APR card or 0% interest purchase card (provided you pay off the balance or transfer it elsewhere by the time the interest-free period expires) are typically the cheapest cards for borrowing.

Compare remortgages

Whether you're looking to save money with a remortgage or borrow more, comparing deals with the help of an expert broker can help you get the best deal for your circumstances.

Remortgaging to release equity FAQs

How long will it take to release equity through remortgaging?

It typically takes four to eight weeks to release equity through remortgaging, however, this does vary depending on the complexity of your circumstances. Make sure you leave yourself enough time to get the funds for whatever you need them for by applying more than eight weeks in advance.

Can I use the equity in my house as a deposit?

Yes, if your equity has increased, you can use it as a deposit, or maybe even buy a home outright if you have enough.

If you 'downsize' and move into a lower value home, you can turn your equity into cash if there is some left over once you’ve bought your new home.

What will happen to my remortgage repayments if I remortgage to release equity?

Of course, if you increase your borrowing, your repayments will also go up. Also bear in mind that the higher your loan to value, the higher the interest rates you’re likely to be offered, so don’t be tempted to release more equity than you need to. You’ll also end up paying more in interest over the life of the loan.

Some of this additional cost may be offset if your new mortgage has a lower interest rate – either because you have a lower LTV due to increased equity, or if interest rates fall generally due to changes in the market.

You could also increase the length of your mortgage term to minimise the increase, but you’ll be paying even more interest overall because you’ll be borrowing the money for longer.