- Uswitch.com>

- Mortgage comparison>

- Best Remortgage Deals And Rates UK 2024

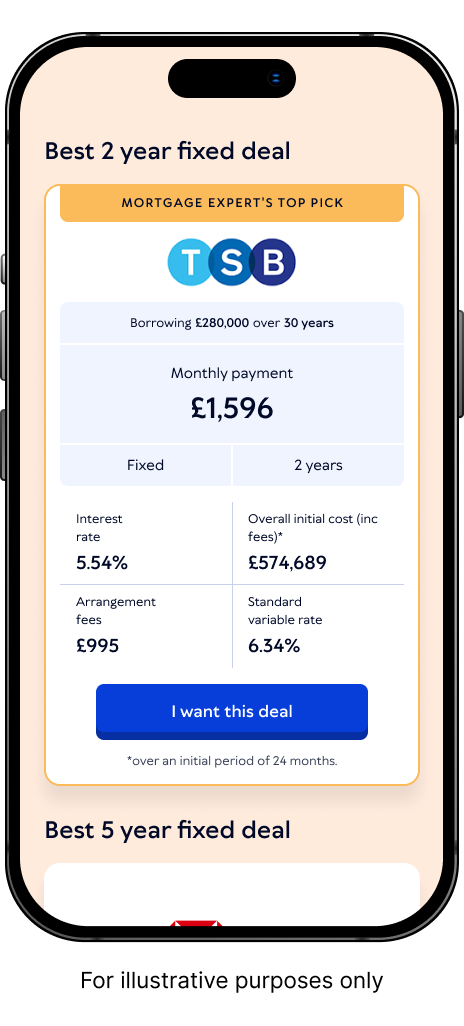

Best remortgage deals & rates

Finding the right remortgage can be a challenge. Should you change lender or stay put?

Let our broker partner, Mojo mortgages, help you to compare remortgage rates and make the right choice for you

How we operate

Our content is regularly reviewed by a team of our expert writers and our services are provided at no cost to you. Learn more about partnership content and how we make our money.

How to compare remortgage rates & deals with Uswitch and Mojo

Add your details

Provide your details so Mojo Mortgages can find remortgage deals that are suited to you and your circumstances

Compare deals with a recommendation

Your Mojo expert will compare the best remortgage deals and call you to recommend those suited to you

Get your mortgage

Your Mojo expert will help you secure your remortgage deal.

Compare remortgage rates from over 70 lenders across the whole of the market

Mojo Mortgages is an award-winning broker. Their expert advisers can look across the market to find the best remortgage deal for you.

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

What does remortgaging mean?

Remortgaging means changing the mortgage deal on your current property. You can either switch your mortgage to a different product with the same lender - known as a product transfer - or choose a new deal with a different lender - usually referred to as a full remortgage.

People mainly remortgage to save money by avoiding their lender's standard variable rate (SVR) when their introductory rate ends. But, you can also change mortgages to borrow more money, using the equity in your home. According to recent buy-to-let statistics, 27% of landlords plan to remortgage a property within the next 12 months, solely for the intention of releasing equity from their portfolios.

Why should I remortgage?

There are multiple reasons why you might benefit from remortgaging - the key is timing, especially if you're looking to get the best remortgage rates available to you.

Here are some of the most common reasons to remortgage:

Remortgage to save money

You've fallen onto your lender’s SVR - often the most expensive rate they have

You've gained equity in your home - This will lower the loan to value (LTV) ratio of your borrowing and the best remortgage rates tend to be available to those with the lowest LTV

Interest rate rises - If you're on a variable rate and see multiple increases to the Bank of England base rate you may begin to crave more stability. Remortgaging to a fixed-rate mortgage in the short term can offer this - even if they are slightly higher initially, they cannot increase until the deal period is over

You want more payment flexibility - certain mortgage products allow larger overpayments with no early repayment charges (ERCs) - this can help you repay your loan earlier. You may also want to consider remortgaging to an offset mortgage if you have substantial savings

Remortgage to borrow more

Some people remortgage to increase their borrowing, which can be helpful in a range of circumstances, such as:

Home improvements

Educational costs

Help kids or other family get onto the property ladder with a deposit

Debt consolidation

Big one-off purchases - car, holiday etc

Keep in mind that remortgaging to release equity (borrow money from the portion of your property you already own) is not always the cheapest way to borrow money.

While mortgage interest rates can be lower than personal loan rates, you pay interest on the additional balance for the entire length of your remaining mortgage term - which is likely to cost more overall.

How do I remortgage?

When you remortgage your property, you essentially pay off your existing mortgage with another mortgage. This can either be with the exact same sized loan, usually at a different rate of interest, or with a larger or smaller loan, depending on your level of equity and what you plan to do.

The application should be similar to taking out your original mortgage, but it's a good idea to take remortgage advice first, to ensure you get the timing right for your circumstances.

Can I get a remortgage deal?

It depends on your current circumstances. When you remortgage your house with another lender, the same eligibility requirements apply as when you took out your original mortgage:

Affordability

Credit status

Age

Property type

LTV - equity in your home should have grown enough to cover a remortgage deposit, but some lenders allow you top up a shortfall with a cash deposit too

If you're concerned that you might not meet the criteria of a new lender, it may be possible to opt for a product transfer instead. Before making a decision on remortgaging, it would be advisable to check out the latest UK remortgage statistics to help select a product that is right for you.

Product transfers are still a form of remortgaging, but with your existing lender. Historically lenders don't reassess finances or credit status to do one, unless you borrow more. However, even the best remortgage deals available are currently higher than they were two, five and ten years ago, so it's possible your affordability will need to be reassessed in some circumstances.

Is remortgaging a good idea?

It depends on your circumstances. If you're about to fall onto an SVR, there's certainly still a significant difference in the remortgage and product transfer rates available, compared to staying put. It's a good idea to get some remortgage quotes, to compare your options.

Taking remortgage advice from a qualified broker, like Mojo Mortgages, is highly recommended before making any decisions of this nature.

Remortgaging in the current market

For many people, the 14 base rate increases in a row over 2022-23 has made remortgaging very difficult. While mortgage current remortgage rates have started to fall again, for the vast majority of people, they're still much higher than when they took out their last mortgage.

In June 2023, The Mortgage Charter was drawn up to assist people struggling with high mortgage costs. It includes the following easements which may help if you're struggling to remortgage:

Mortgage holders can switch to interest-only repayments for up to six months to reduce their monthly payments - rates may be more affordable to you after this period

Mortgage terms can be extended up to 40 years (for six months)

Customers who are up to date with their repayments may product transfer onto a fixed-rate deal with their current lender

No affordability checks or credit checks will be carried out to set up these temporary measures

Keep in mind: All options above have the potential to impact your long-term financial circumstances, even if they help in the short term.

When should I remortgage?

Timing is the key to maximising the benefits of remortgaging, but the best time to remortgage will depend on your individual circumstances.

For example, if you're coming to the end of your current fixed-rate deal or variable rate introductory deal period - you can set up a remortgage as far as six months in advance of the end date.

On the other hand, if your financial circumstances have changed for the worse, it could be difficult to qualify for a remortgage. This is especially in the current climate, when remortgage rates have risen dramatically and people are struggling to meet affordability requirements to remortgage.

The Mortgage Charter could help you in the short term if you're trapped on a high SVR and unable to remortgage.

Why get a remortgage comparison through Uswitch?

"We had to remortage as our current term was coming to an end. The whole process was so easy and informative, from the first questionnaire through to the appointment and consultation. Felt we were well advised, no pressure selling. Overall a very stress free experience and ended with up a much better deal than we thought we would get."

Trustpilot review, Mojo Mortgages customer - 8th February 2024

What are remortgage rates?

Remortgage rates vary from one deal to the next and one lender to another. Current remortgage rates are fairly high when compared with recent years, but around average when looking at the longer term history of remortgage deals in the UK.

The SVR (standard variable rate) that you fall onto when a fixed or variable rate introductory period ends, are typically among the highest rates offered by lenders. It's a good idea to look at remortgage quotes around six months ahead of your deal expiry date.

What are current remortgage rates in the UK?

Remortgage rates tend to be bespoke to the applicant, depending on circumstances such as:

Financial circumstances

Credit score

Equity held in property

Generally interest rates have started to fall gradually after peaking in September 2023. The cheapest remortgage rates are generally available to those with the greatest equity in their home. You can keep up with current average mortgage rates on our mortgage rates today page.

How to find the best remortgage deals

The best remortgage deals are available to those with the lowest LTV (so the greatest level of equity in their home).

However, the cheapest remortgage rates won't always reflect the best deal over all. Remember to also consider fees when calculating the overall cost of switching deals.

Our broker partner Mojo Mortgages has access to the latest rates available, and can carry out a full comparison of remortgage deals across the whole market on your behalf.

What are the fees for remortgaging?

Remortgaging is essentially taking out another mortgage - so most of the fees involved in taking out a mortgage will still apply. This could include any or all of the following:

Exit fees to leave

ERCs if you leave before the deal end date

Arrangement fees

Legal fees

Valuation fees

What are the disadvantages of remortgaging?

There are a few potential disadvantages to remortgaging, although, much like the benefits, your circumstances will have a big impact on whether they impact you, and to what extent:

Usually you'll need to pay remortgage fees, which can get costly if you remortgage every 2 or 5 years throughout the full duration of the mortgage - sometimes cancelling out the financial benefits

Not everyone is able to remortgage when they want to, as it can be difficult to qualify, especially with current remortgage rates higher than when most people remortgaging at the moment took out their deal. It can also be difficult if your financial circumstances decline

Remortgaging can take time, it's often quicker to do a product transfer

A new lender may not always be the right fit, especially if you're happy with your existing one

If you try to remortgage while still in an introductory or fixed rate period, you may have to pay additional charges know as ERCs

If your mortgage deal is ending within the next six months, you should look at remortgage options asap. Remortgage rates are fleeting right now, so it's a good idea to speak to a broker and lock in the best rates while you can. ”Kellie Steed, Mortgage Content Writer

Customer Reviews

I would definitely recommend Mojo…

Very positive experience

Quick remortgage work

Remortgage FAQs

Can I get a new mortgage with a different lender?

Yes, you can, so long as you are able to meet the criteria.

The process tends to be lengthier than transferring to a new deal with your current lender (a product transfer). Providers sometimes offer better deals to existing customers, but you could save more by remortgaging with a different lender, so it’s worth comparing all the deals available.

How much can I borrow when I remortgage?

When you remortgage your house, you can either borrow the remaining outstanding balance on your mortgage - usually if you're just changing deals for a cheaper rate or to switch to a new fixed remortgage deal because your previous term has ended.

You may also be able to borrow more when you remortgage, but this will depend on your circumstances. Having more equity in your home can make it easier to borrow additional money when you remortgage, but you'll also need to prove you can afford to repay the larger amount.

Why remortgage with a broker?

Remortgage comparisons can be difficult to manage alone, due to the high volume of deals available. Not to mention the fact the every lender has a different set of criteria that you will need to meet. Rates are also changing incredibly quickly in the current market, so deals seen online are not always available by the time you apply.

Mortgage brokers with access to the whole market, like those at Mojo, know which lenders can offer the best remortgage rates for your circumstances. They also have access to deals you won't necessarily see online.

How long does it take to remortgage?

Remortgaging usually takes about a month, which is the time you need to complete all the paperwork and have a valuation carried out on your home. When the process is over, you’ll be notified with a completion statement from your lender.

If you choose to remortgage with the same lender, this is known as a product transfer. Because the lender already has all your details, product transfers tend to be quicker than remortgaging with a new lender. Some lenders offer digital product transfers which can be completed online very quickly.

Will I have to pay an early repayment charge?

If you’re still locked into a mortgage deal, it’s likely you’ll have to pay an early repayment charge (ERC). An ERC is a penalty for leaving your existing mortgage deal early. It’s usually calculated as a percentage of the amount borrowed, which tends to decrease the closer to the end of the deal you get.

Paying an ERC to remortgage before your fixed-rate period comes to an end could take any savings you would make. So make sure you calculate the costs carefully to decide whether it's worth it for you.

Can I remortgage from interest-only to a capital repayment mortgage?

Most lenders won’t need you to remortgage in order to change from an interest-only to a capital repayment mortgage deal with them. In fact, they will usually be happy for you to do this, as it reduces the risk to them.

If you wanted to change from a repayment to an interest-only mortgage your options would be reduced, as not all lenders are happy to offer interest-only mortgages for residential homes. However, you may be able to do so as a temporary option under the mortgage charter.

Will applying for a remortgage affect my credit score?

Mortgage lenders carry out a credit check at mortgage application to decide whether to lend to you. If this is a ‘hard search’, which it typically will be at application stage, it leaves a mark on your credit score temporarily, but this shouldn’t affect it too much.

The real problem is where you make multiple applications to a number of lenders before being accepted. This makes it obvious that you have been declined by others, but also gives the appearance of desperation, which can discourage future lenders from approving your remortgage application.

The best way to avoid this is to speak to a broker who will be able to direct you to those lenders whose criteria you are most likely to meet.

Will I need to have my house valued when I remortgage?

If you remortgage with a new lender, you will need to have a property valuation. Much like you did when you took out the original mortgage.

If you use a product transfer to remortgage with your current lender, you won’t usually need to have a valuation, however, you may need to if your house has changed significantly in value.

Can I remortgage if I'm self-employed?

Yes, you can. This will typically be easier if you had the same circumstances when you took out your original mortgage, or have been self-employed for a substantial period of time, however.

Self employed mortgage applicants will usually need to demonstrate a lengthier period of stable income than employed applicants, with two to three years of accounts and tax calculations the standard requirement. There are a few lenders who will look at self-employed applicants with as little as 12 months trading history, however.

Can I remortgage with bad credit?

Yes, it’s certainly possible, depending on the level of your credit issue. There are bad credit lenders specifically intended to help people in these circumstances, although the remortgage rates tend to be higher.

If you’re concerned about your credit score, another option is to consider a product transfer. Your existing lender is unlikely to check your credit rating or affordability unless you’re increasing your loan amount or extending the term of your mortgage, so a product transfer can be an easier option.

How does the LTV of my property affect remortgaging?

Lenders have a maximum LTV that they are willing to offer in any given scenario, depending on how well you meet the other lending criteria and how much you need to borrow.

As lower LTV borrowing is less of a risk to the lender, the interest rates offered tend to be more competitive.

The LTV is the percentage of the total cost of the property that you need to borrow. To calculate it, find out the total outstanding value of your mortgage, your property’s current value and then divide your outstanding mortgage balance by your property’s value:

Example:

You have £100,000 left to pay on your mortgage

Your property is worth £200,000

Divide £100,000 by £200,000

= 0.50.5 x 100 = 50 (or 50% LTV)

When you remortgage, the LTV will depend on:

How much of the original loan you have repaid

Whether your property has increased in value and;

Whether you need to borrow more money or are simply remortgaging for a better interest rate

Can I remortgage as an older borrower?

Historically older borrowers have had a harder time remortgaging, especially if they are nearing retirement age, due to the maximum age limits imposed by many lenders.

However, in recent years there has been a noticeable increase in flexibility in this area, with some lenders extending their maximum age of borrower and maximum age by which the mortgage needs to be repaid.

When nearing retirement age, many people reassess their finances, and a large part of this is likely to be looking at their remaining mortgage balance, and how they can live more comfortably in their later years.

People in these circumstances may consider more specialist products, such as:

Remortgaging onto a retirement interest-only mortgage (RIO) - often a helpful option for homeowners likely to fall short of repaying the final lump sum balance on an interest-only mortgage.

Remortgage onto an equity release product - always take qualified financial advice from an equity release specialist before considering this type of remortgage.

Will I need to arrange a solicitor or conveyancer when I remortgage?

If you're changing lenders, yes you will - although some lenders offer free conveyancing services as part of your remortgage deal.

A conveyancing solicitor is required for a full remortgage, but not for a product transfer, as the debt will not change hands when you remortgage with the same lender.

How early can I remortgage?

You can, theoretically, remortgage after 6 months of having most mortgages. There is no legal requirement to stay in a deal period, even if you choose a fixed remortgage deal. However, it's weighing up when you can do so without paying a fee that's important.

ERCs (early repayment charges) tend to apply if you leave a fixed length mortgage deal before the end date.

How soon can I remortgage before the fixed-rate ends?

If your deal has a tie in period, whether that's a fixed rate or an initial deal period on a variable rate deal, you'll usually need to pay ERCs in order to leave before it ends.

It is, however, possible select a new deal around six months in advance of that end date. So if you see a cheap remortgage deal, you can lock in that rate and it will automatically begin when your original deal ends. And because you don't leave until it does, you won't have any ERCs to pay.

How does remortgaging work?

When you remortgage, you simply switch your mortgage loan to a different deal. This works by paying off your outstanding balance with the new loan funds, and then repaying the new loan monthly, instead of the old one.

About the author

Didn’t find what you were looking for?

Find out about other mortgages

Read some of our most popular guides

We’ve been featured in

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions. Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website. Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH. Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215) Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH, and head office is WeWork No. 1 Spinningfields, Quay Street, Manchester, M3 3JE. To contact Mojo by phone, please call 0333 123 0012.