Providers charge per-transaction fees, often including fixed costs and percentages of each transaction. Consider setup and monthly fees when choosing a provider based on your business size and transaction volume.

Find the best card machine for your business

89% of businesses who switch save on their card machine costs

Save between £100 and £450* per month

Receive your new card machine and start taking payments within 48 hours

*The NFRN estimated its members saved between £100 and £450 per month when switching card acceptance service providers. Larger businesses may save more. Savings are indicative and will vary based on merchant information provided to Tuza.

How it works

89% of business who switch save on their card machine costs - here's how

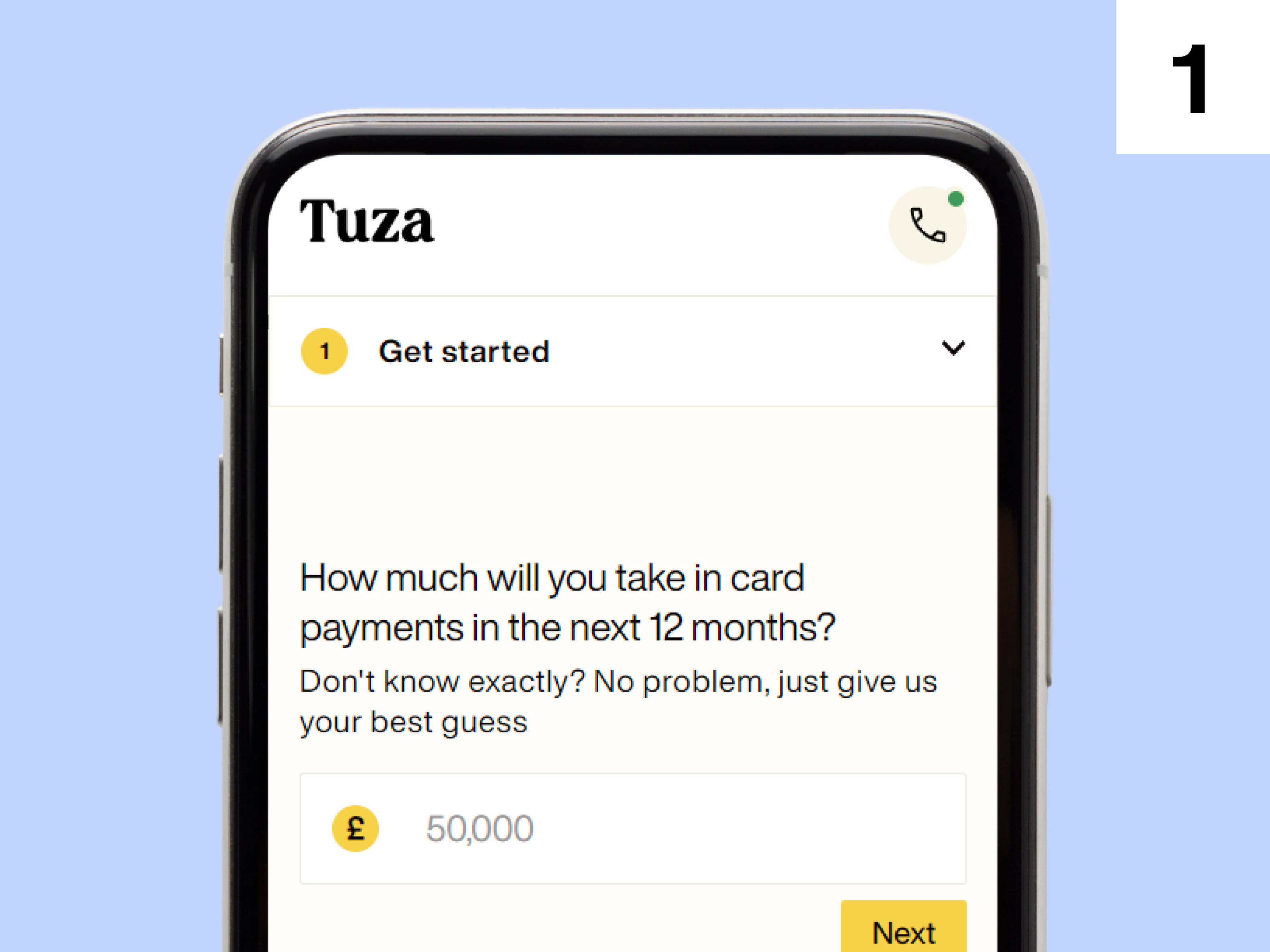

Answer a few simple questions about your business

Compare card payment machines from leading providers

Switch and start saving today

Simplifying card payments for small businesses

Whether you're looking for your first card machine or ready to upgrade, Tuza makes it easy to compare card payment machines or switch to the best provider.

Unlock exclusive rates from the UK's leading providers

Find a card payment machine that suit your needs

Get the best rates and save more on your transactions

What are payment providers?

Payment providers enable businesses to accept payments from customers, be it online or in-person.

They typically process credit and debit card transactions but may also offer alternative payment options like open banking or buy now, pay later (BNPL).

Examples of payment providers on Tuza include Barclaycard, Worldpay, Revolut and SumUp.

Why is it important to compare card payment providers?

Comparing card payment providers helps you find the best deal for your business.

Fees, features, and technology can vary widely between providers, so reviewing your options ensures you’re not overpaying for what you need and that you're using the most efficient, up-to-date system for processing payments.

What payment methods can I accept?

Card-based payments

This category includes credit cards, debit cards, and prepaid cards. These types of payments are often processed via networks such as Visa, MasterCard, American Express, Discover etc. They are widely used for both online and in-person transactions.

Bank payments

This method includes payments made directly from one bank account to another. This method is often used for recurring payments like bills or subscriptions.

Digital payments

This is a broad category that includes all payments made using digital or mobile technology. This can include app-based services like PayPal, Google Pay, and Apple Pay. It can also include mobile payments made using contactless technology or QR codes.

What information does Tuza need about my business?

To give you an accurate quote, Tuza just needs a few key details – and it only takes a couple of minutes.

You’ll be asked about:

your annual card turnover

your average transaction value

the nature of your business.

Tuza will also want to know how and where you take payments (online, in-person, or both), which payment methods you accept, who your customers are, and what types of cards they typically use (debit, credit, or business).

Key things to remember when searching for a payment provider

Fees

Providers charge per-transaction fees, often including fixed costs and percentages of each transaction. Consider setup and monthly fees when choosing a provider based on your business size and transaction volume.

Speed of processing

Find out how quickly the payment provider can process transactions and deposit funds into your bank account. While some providers offer same-day or next-day deposits, others might take longer.

Acceptance of different cards

Ensure the provider can process a variety of cards, including Visa, MasterCard, and American Express.

Integration

How well does the provider's system integrate with your existing infrastructure, such as your POS system, online store, or accounting software? Smooth integration can help reduce administrative burdens and ensure a better experience for your customers.

Security

The payment provider should comply with all relevant security standards, including the Payment Card Industry Data Security Standard (PCI DSS). This helps ensure the security of your customers' card information.

Flexibility and scalability

Ideally, the payment provider should be able to support your business as it grows and evolves. This could include the ability to handle increased transaction volumes, support for multi-currency transactions if you expand internationally, or additional services like invoicing or recurring billing.

Fraud protection

Some payment providers offer tools and services to help you detect and prevent fraudulent transactions. This can help protect your business and your customers.

Contract terms

Be sure to understand the length of the contract and any penalties for early termination.

Customer support

Reliable and responsive customer service is crucial. Check if the provider offers support 24/7, and consider looking at reviews to see how well they handle customer issues.

Key things to remember when searching for a payment provider

Fees

Speed of processing

Find out how quickly the payment provider can process transactions and deposit funds into your bank account. While some providers offer same-day or next-day deposits, others might take longer.

Acceptance of different cards

Ensure the provider can process a variety of cards, including Visa, MasterCard, and American Express.

Integration

How well does the provider's system integrate with your existing infrastructure, such as your POS system, online store, or accounting software? Smooth integration can help reduce administrative burdens and ensure a better experience for your customers.

Security

The payment provider should comply with all relevant security standards, including the Payment Card Industry Data Security Standard (PCI DSS). This helps ensure the security of your customers' card information.

Flexibility and scalability

Ideally, the payment provider should be able to support your business as it grows and evolves. This could include the ability to handle increased transaction volumes, support for multi-currency transactions if you expand internationally, or additional services like invoicing or recurring billing.

Fraud protection

Some payment providers offer tools and services to help you detect and prevent fraudulent transactions. This can help protect your business and your customers.

Contract terms

Be sure to understand the length of the contract and any penalties for early termination.

Customer support

Reliable and responsive customer service is crucial. Check if the provider offers support 24/7, and consider looking at reviews to see how well they handle customer issues.

Join the millions who have already switched.

More people switch their broadband and mobile with us than any other switching site.

Here's what some of our customers have to say:

Customer Reviews

by 39,363 people

Very simply to change

Very simply to change. Easy to see the difference between tariffs.

Ricardo Ve

Simple System

So easy and quick to use the system.

Leslie Waelend

Good data

Great service - pain free

Mr Williamson