Remortgage calculator

Find out how much you could save by remortgaging with the same or a different lender.

Finding the right remortgage deal can be a challenge. Should you change lender or stay put?

To help you navigate this, consider a remortgage comparison call with our expert broker partner, Mojo Mortgages. They’ll compare the latest remortgage rates available, helping you to make the right choice for your needs.

Remortgaging means changing your mortgage without changing your home. Sometimes you can switch your mortgage to a different product with your existing lender (known as a product transfer) or you can select another mortgage product with an entirely different lender (known as a remortgage).

There are a wide variety of reasons that people may choose to remortgage their home, but often they want to save money or borrow more money.

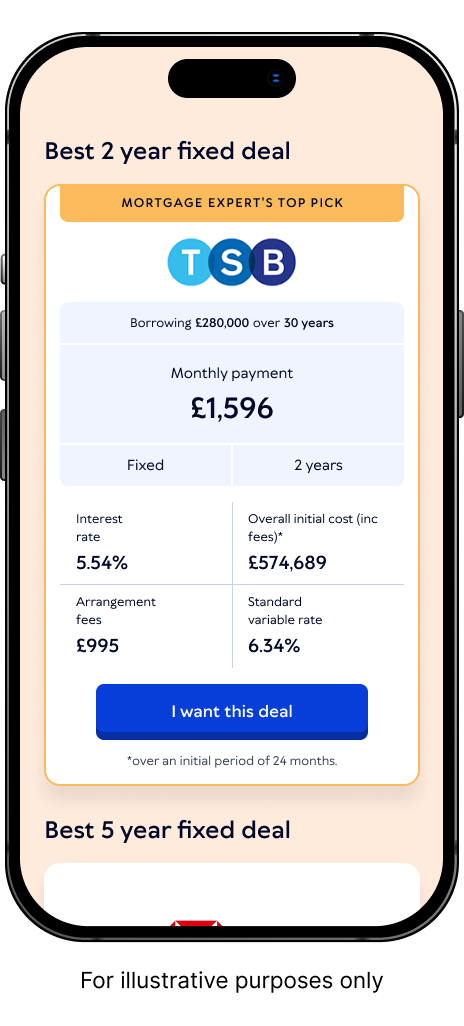

This table shows some of our partner Mojo's best 2 year and 5 year fixed remortgage deals based on their initial rates available at different loan-to-value (LTV) ratios. This initial rate is what you pay throughout the introductory period (for a 2 year fixed-rate mortgage, the introductory period is two years).

The APRC (Annual Percentage Rate of Change) is included after each initial rate. APRC provides an overall picture of the mortgage deal, taking fees and the lender's standard variable rate (SVR) you typically fall onto after the introductory period into account.

This can be useful when comparing different mortgage deals, but doesn't consider that many people remortgage onto another deal before they move onto the SVR.

Your property may be repossessed if you do not keep up with your mortgage repayments.

| LTV | Best 2 year fixed rate remortgages | Best 5 year fixed rate remortgages |

|---|---|---|

| 90% | Bank Of Ireland Initial rate: 5.03% | APRC: 6.9% Repayment mortgage of £270,000.00 over 25 years, representative APRC 6.9%. Repayments: 27 months of £1,581.51 at 5.03% (fixed), then 273 months of £1,873.98 at 6.94% (variable). Total amount payable £554,297.31. Early repayment charges apply until 31-Oct-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £3205. | HSBC Initial rate: 4.98% | APRC: 5.9% Repayment mortgage of £270,000.00 over 25 years, representative APRC 5.9%. Repayments: 63 months of £1,573.66 at 4.98% (fixed), then 237 months of £1,743.30 at 6.24% (variable). Total amount payable £512,302.68. Early repayment charges apply until 31-Oct-2031. Arrangement, mortgage discharge, valuation and CHAPS fees total £999. |

| 80% | Bank Of Ireland Initial rate: 4.69% | APRC: 6.8% Repayment mortgage of £240,000.00 over 25 years, representative APRC 6.8%. Repayments: 27 months of £1,360.01 at 4.69% (fixed), then 273 months of £1,663.17 at 6.94% (variable). Total amount payable £490,765.68. Early repayment charges apply until 31-Oct-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1205. Legal fees £258. | Bank Of Ireland Initial rate: 4.75% | APRC: 6.3% Repayment mortgage of £240,000.00 over 25 years, representative APRC 6.3%. Repayments: 63 months of £1,368.28 at 4.75% (fixed), then 237 months of £1,631.16 at 6.94% (variable). Total amount payable £472,786.56. Early repayment charges apply until 31-Oct-2031. Arrangement, mortgage discharge, valuation and CHAPS fees total £1205. Legal fees £258. |

| 70% | Bank Of Ireland Initial rate: 4.45% | APRC: 6.8% Repayment mortgage of £210,000.00 over 25 years, representative APRC 6.8%. Repayments: 27 months of £1,161.30 at 4.45% (fixed), then 273 months of £1,452.73 at 6.94% (variable). Total amount payable £427,950.39. Early repayment charges apply until 31-Oct-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1705. Legal fees £258. | Bank Of Ireland Initial rate: 4.54% | APRC: 6.2% Repayment mortgage of £210,000.00 over 25 years, representative APRC 6.2%. Repayments: 63 months of £1,172.02 at 4.54% (fixed), then 237 months of £1,422.05 at 6.94% (variable). Total amount payable £410,863.11. Early repayment charges apply until 31-Oct-2031. Arrangement, mortgage discharge, valuation and CHAPS fees total £1705. Legal fees £258. |

| 60% | Bank Of Ireland Initial rate: 4.45% | APRC: 6.8% Repayment mortgage of £180,000.00 over 25 years, representative APRC 6.8%. Repayments: 27 months of £995.40 at 4.45% (fixed), then 273 months of £1,245.20 at 6.94% (variable). Total amount payable £366,815.40. Early repayment charges apply until 31-Oct-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1705. Legal fees £258. | Bank Of Ireland Initial rate: 4.54% | APRC: 6.2% Repayment mortgage of £180,000.00 over 25 years, representative APRC 6.2%. Repayments: 63 months of £1,004.59 at 4.54% (fixed), then 237 months of £1,218.90 at 6.94% (variable). Total amount payable £352,168.47. Early repayment charges apply until 31-Oct-2031. Arrangement, mortgage discharge, valuation and CHAPS fees total £1705. Legal fees £258. |

The above fixed rates are provided by Mojo Mortgages and updated every 12 hours. THEY MAY NOT BE AVAILABLE WHEN YOU'RE READY TO SUBMIT AN APPLICATION.

There are several reasons why you might want to remortgage:

There are a number of ways you could make both short-term and longer-term savings by shopping around remortgage deals:

This rate is usually higher than other deals available so at this point, people often look at the best remortgage deals available to them, to see if they could save on their existing rate

If you've gained substantial equity in your home, the loan to value (LTV) ratio of your borrowing will have reduced. This means that the percentage of your borrowing has fallen compared to the cost of the property. As the best remortgage rates tend to be available to those with the lowest LTV, this might be a good time to look at your options

You're on a variable rate deal and there are increases in the Bank of England base rate, you may feel the need for more stability with your repayments. A fixed-rate mortgage can give you peace of mind, as the interest rate cannot increase until the fixed-rate period is over.

One way to save money on your mortgage in the longer term is to repay it more quickly, as this reduces the total amount of interest you'll pay over the mortgage term. Some mortgages allow overpayments of up to 10% of the loan per year, but if you want to overpay more you might consider remortgaging to a deal with more flexible terms. An offset mortgage can also help you to pay your mortgage off sooner

Some people remortgage to increase their borrowing, which can be helpful in a wide variety of circumstances:

To carry out home improvements

To pay for the costs of education or help get family members onto the property ladder

To consolidate debts

For large purchases, such as a car or holiday

It’s worth taking into consideration that this is not always the cheapest way to borrow money. While mortgage interest rates can be lower than those on a personal loan, you'll be paying interest on that additional balance for the entire length of your remaining mortgage term.

It depends on your current circumstances. When you remortgage your house with another lender, the same eligibility requirements apply as when you took out your original mortgage:

Affordability

Credit status

Age

Property type

LTV - equity in your home should have grown enough to cover a remortgage deposit, but some lenders allow you top up a shortfall with a cash deposit too.

The optimal time to remortgage is usually around three to six months before your current deal comes to an end. This allows you to compare remortgage deals and secure a new rate, avoiding being automatically moved onto your lender’s standard variable rate.

If you want to remortgage sooner, you’ll likely need to pay early repayment charges to leave your current deal early. That said, remortgaging sooner might be worthwhile if:

Lower interest rates are available (as long as paying any early repayment charges won’t outweigh the benefits of the better rate)

Your property value has substantially increased, giving you access to more competitive rates

Your financial needs have changed, so you need to adjust your mortgage term or move to a lender that offers better flexibility

You want to release equity and remortgage to borrow more money

You’re coming to the end of your current fixed-rate deal or introductory deal period - you can set up a remortgage as far as six months in advance of the end date

You see a much better rate - bear in mind that you'll need to look at how much any early repayment charges (ERCs) will cost you to leave your existing deal, as they could outweigh the benefits of the better rate

You’re on a variable rate deal and the Bank of England base rate looks like it will rise soon - remortgaging to avoid increased interest rates may be possible, so long as your ERCs won’t end up costing you more

Your home has increased in value dramatically, reducing your LTV

Your current lender doesn’t offer the flexibility you would like, such as offsetting or the ability to overpay

You’re not tied into a deal that has ERCs to pay so can leave at any time

If there are no better rates available than your existing one, in which case it’s probably not worth paying the fees involved with remortgaging, especially if you also have ERCs to pay

If you’re only a short way into a fairly long fixed period. The further you are from the end of your fixed or introductory rate term, the higher fees are likely to be. It’s unlikely you will benefit from remortgaging at this point, but ERCs tend to decrease the closer you are to the end of the deal

Your property value has fallen, causing your LTV to increase, or worse, putting you in negative equity (where you owe more than the current value of your home). If you're in negative equity, it's unlikely you'd be able to secure a remortgage

If you haven’t gained much equity in your home yet, as your property value hasn’t increased and you haven’t repaid much of the original loan. Lenders usually have a minimum equity requirement to remortgage

Your financial circumstances have changed for the worse, meaning that it would be difficult to qualify for a remortgage. You may still be able to do a product transfer with your existing lender, so long as you don’t want to borrow more

Remortgage rates vary from one deal to the next and one lender to another, but are usually competitive compared to the SVR (standard variable rate) that you fall onto when a fixed or variable rate introductory period ends.

These are typically among the highest rates offered by lenders, so it's a good idea to look at remortgage quotes around six months ahead of your deal expiry date.

Remortgage rates tend to be bespoke to the applicant, depending on circumstances such as:

Financial circumstances

Credit score

Equity held in property

The cheapest remortgage rates are generally available to those with the greatest equity in their home. Keep up to date with today's current remortgage rates and speak to a broker to ensure you secure the best rate for you.

The best remortgage deals are available to those with the lowest LTV (so the greatest level of equity in their home).

However, the cheapest remortgage rates won't always reflect the best deal over all. Remember to also consider fees when calculating the overall cost of switching deals.

Our broker partner Mojo Mortgages has access to the latest remortgage rates available, and can carry out a full comparison of remortgage deals across the whole market on your behalf.

Remortgaging is essentially taking out another mortgage - so most of the fees involved in taking out a mortgage will still apply. This could include any or all of the following:

Exit fees to leave

ERCs if you leave before the deal end date

Arrangement fees

Legal fees

Valuation fees

Remortgaging typically includes researching and comparing deals, assessing how much you need to borrow, getting an agreement in principle, completing the full mortgage application, getting a property valuation and using a conveyancer to support you with the legal transfer to the new mortgage.

Remortgaging with a new lender usually takes several weeks though, if you stick with the same lender, you may find the process much quicker.

The remortgaging timeline looks like this:

Research and comparison - Once you’ve compared the latest remortgage deals, your next step is often deciding whether to go it alone or speak with a mortgage broker. A fee-free broker can do the heavy lifting for you, scouring the market to find a deal tailored to your specific financial situation. However, it pays to keep your eyes open - while some "intermediary only" deals are exclusive to brokers, other "direct only" rates can only be found by going straight to the lender.

Remortgage Application - If you decide to switch to a new lender, be prepared for a bit of admin. You’ll typically need to hand over "the big three" - proof of ID, your most recent payslips, and several months of bank statements so they can run their affordability checks. However, if you stick with your current lender for a product transfer, the process is often much smoother. Since they already know your financial history, you might find you don't need to provide all that paperwork again, making the jump to a new deal significantly faster.

Lender Checks - Lenders will run a thorough affordability check, weighing your income against your monthly outgoings to ensure you can afford the repayments. They’ll also review your credit history, check your credit rating and conduct a property valuation to confirm the home is worth the loan amount they're offering to lend you.

Mortgage Offer & Completion - Once the lender approves your application, they’ll issue a formal mortgage offer. Once accepted, your solicitor or conveyancer takes over to handle the legal paperwork and finalise the deal. On the day of completion, your new lender sends the funds directly to your old provider to pay off the existing debt, with any additional borrowing you've requested paid straight to you.

Some mortgage brokers will charge you a fee for comparing remortgaging options and offers. But don’t worry - our broker partner, Mojo Mortgages, offers a completely free service to help you get remortgage quotes.

The current Bank of England (BoE) base rate was held 3.75% on 18 June 2026 after a 25 basis point cut from 4% in December 2025. While there are no guarantees when it comes to how this might impact mortgage rates, this may be positive news for some homeowners looking to remortgage. Those remortgaging may be wondering whether to opt for a two or five year fixed rate, with industry analysts suggesting that mortgage rates are currently falling faster for shorter-term fixes.

In a remortgage, you can remortgage with the same lender, known as a product transfer (or mortgage renewal), or switch to a new deal. To see how the numbers stack up, chat with a broker to get a personalised remortgage quote.”Laura Hamilton, Mortgage Expert

When deciding whether to remortgage, navigating your options can sometimes feel overwhelming. Here are just some of the advantages of remortgaging to consider:

You may be able to access more competitive rates when remortgaging, particularly if you’re about to fall onto an SVR, which typically carries higher interest rates

You can choose from a few different remortgaging options. For example, a product transfer may be quicker and more straightforward than remortgaging with a new lender

If you’re looking to borrow more money, you may find that remortgaging to use the equity in your property is a suitable borrowing option for you

You may be able to change the term on your mortgage. Depending on your financial goals, this could either reduce your monthly payments (though it will cost more interest in total) or reduce the total amount of interest you pay (though you’ll likely be faced with higher monthly payments)

If your current mortgage deal no longer suits your needs, remortgaging can help you find a product that better aligns with your financial goals (for example, moving to a lender who has a more flexible approach to overpayments)

If your financial situation has changed for the better since you first took out your mortgage, you may qualify for better rates

There are a few potential disadvantages to remortgaging, although, much like the benefits, your circumstances will have a big impact on whether they impact you, and to what extent:

Usually you'll need to pay remortgage fees, which can get costly if you remortgage every 2 or 5 years throughout the full duration of the mortgage - sometimes cancelling out the financial benefits

Not everyone is able to remortgage when they want to, as it can be difficult to qualify, especially with current remortgage rates higher than when most people remortgaging at the moment took out their deal. It can also be difficult if your financial circumstances decline

Remortgaging can take time, it's often quicker to do a product transfer

A new lender may not always be the right fit, especially if you're happy with your existing one

If you try to remortgage while still in an introductory or fixed rate period, you may have to pay additional charges know as ERCs

Remortgage rates tend to be bespoke to the applicant, depending on circumstances such as:

Your financial circumstances

Your credit history

How much equity is held in property

The cheapest remortgage rates are generally available to those with the greatest equity in their home (i.e. the lowest loan-to-value).

Speaking to a broker can help you secure the best rate for you. Our broker partner Mojo Mortgages has access to the latest remortgage rates available, and can carry out a full comparison of remortgage deals across the whole market on your behalf.

Remortgaging is essentially taking out another mortgage - so most of the fees involved in taking out a mortgage will still apply. This could include any or all of the following:

Exit fees to close your mortgage account with your current lender

Early repayment charges if you leave before the deal end date

Arrangement fees, paid to the new lender for setting up your mortgage

Legal fees to cover the legal work involved in switching mortgages

Valuation fees so your lender can assess the property’s value

Booking fees, charged by some lenders when you apply for a mortgage

Deeds release fee to cover the costs of your lender sending over the title deeds to your solicitor

Some lenders will offer to pay your conveyancing fees or valuation fees as an incentive for switching to them. So it’s important to consider all additional fees when comparing remortgage deals to understand the overall cost.

Find out how much you could save by remortgaging with the same or a different lender.

Your property may be repossessed if you do not keep up repayments on your mortgage.

If your mortgage deal is ending within 6 months, speak to a broker to lock in your best remortgage rates asap. You're not bound to the new remortgage deal until your existing one ends, so the earlier the better.”Laura Hamilton, Mortgage Expert

My experience was perfect very helpful…

Great company and rates

Thank you

Lenders have a maximum LTV that they are willing to offer in any given scenario, depending on how well you meet the other lending criteria and how much you need to borrow.

As lower LTV borrowing is less of a risk to the lender, the interest rates offered tend to be more competitive.

The LTV is the percentage of the total cost of the property that you need to borrow. To calculate it, find out the total outstanding value of your mortgage, your property’s current value and then divide your outstanding mortgage balance by your property’s value:

Example:

You have £100,000 left to pay on your mortgage

Your property is worth £200,000

Divide £100,000 by £200,000

= 0.50.5 x 100 = 50 (or 50% LTV)

When you remortgage, the LTV will depend on:

How much of the original loan you have repaid

Whether your property has increased in value and;

Whether you need to borrow more money or are simply remortgaging for a better interest rate

When you remortgage your house, you can either borrow the remaining outstanding balance on your mortgage - usually if you're just changing deals for a cheaper rate or to switch to a new fixed remortgage deal because your previous term has ended.

You may also be able to borrow more when you remortgage, but this will depend on your circumstances. Having more equity in your home can make it easier to borrow additional money when you remortgage, but you'll also need to prove you can afford to repay the larger amount.

Remortgaging usually takes about a month, which is the time you need to complete all the paperwork and have a valuation carried out on your home. When the process is over, you’ll be notified with a completion statement from your lender.

If you choose to remortgage with the same lender, this is known as a product transfer (or mortgage renewal). Because the lender already has all your details, product transfers tend to be quicker than remortgaging with a new lender. Some lenders offer digital product transfers which can be completed online very quickly.

If you remortgage with a new lender, you will need to have a property valuation. Much like you did when you took out the original mortgage.

If you use a product transfer to remortgage with your current lender, you won’t usually need to have a valuation, however, you may need to if your house has changed significantly in value.

Historically older borrowers have had a harder time remortgaging, especially if they are nearing retirement age, due to the maximum age limits imposed by many lenders.

However, in recent years there has been a noticeable increase in flexibility in this area, with some lenders extending their maximum age of borrower and maximum age by which the mortgage needs to be repaid.

When nearing retirement age, many people reassess their finances, and a large part of this is likely to be looking at their remaining mortgage balance, and how they can live more comfortably in their later years.

People in these circumstances may consider more specialist products, such as:

Remortgaging onto a retirement interest-only mortgage (RIO) - often a helpful option for homeowners likely to fall short of repaying the final lump sum balance on an interest-only mortgage.

Remortgage onto an equity release product - always take qualified financial advice from an equity release specialist before considering this type of remortgage.

Yes, it’s certainly possible, depending on the level of your credit issue. There are bad credit lenders specifically intended to help people in these circumstances, although the remortgage rates tend to be higher.

If you’re concerned about your credit score, another option is to consider a product transfer. Your existing lender is unlikely to check your credit rating or affordability unless you’re increasing your loan amount or extending the term of your mortgage, so a product transfer can be an easier option.

Choosing between a product transfer (or mortgage renewal) with your current lender or remortgaging to a new lender depends on lots of factors including interest rates, fees and your financial goals.

Switching lenders

You may be able to access more competitive interest rates from a new lender

A new lender may offer different features, such as the ability to overpay

You’ll be able to borrow more if you choose to

Product transfer

Often quicker and simpler, with no legal work involved or property valuation needed

Avoids potential exit fees from your current lender

May be a better option if your financial situation has changed and switching lenders would be difficult

There’s no one right answer for all. Be sure to weigh up your options and discuss the different fees and deals with a mortgage broker.

Find out about other mortgages

Read some of our most popular guides

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions.

Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website.

Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH.

Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215)

Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH. To contact Mojo by phone, please call 0333 123 0012.