- Uswitch.com>

- Mortgages>

- Best 2 Year Fixed Rate Mortgages

Compare 2 year fixed rate mortgages

Tell us about yourself and use an expert comparison call with our broker partner Mojo to find your best 2-year fixed-rate mortgage deal from the latest rates in July 2026

How we operate

Our content is regularly reviewed by a team of our expert writers and our services are provided at no cost to you. Learn more about partnership content and how we make our money.

Here’s how to compare 2 year fixed rate mortgages with us

Tell us your mortgage needs

Get a recommendation from across 1000s of 2 year fixed rate mortgage deals

Secure more than just a 2 year fixed rate mortgage offer

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

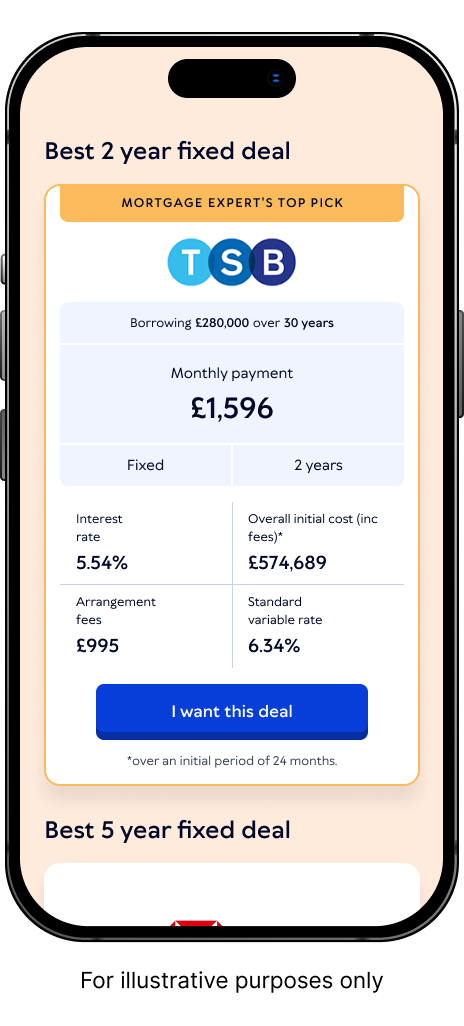

Best 2 year fixed mortgage rates

This table shows some of our partner Mojo's best two-year fixed-rate mortgage deals based on their initial rates available at different loan-to-value (LTV) ratios. This initial rate is what you pay throughout the introductory period (for a two-year fixed-rate mortgage, the introductory period is two years).

The APRC (Annual Percentage Rate of Change) is included after each initial rate. APRC provides an overall picture of the mortgage deal, taking fees and the lender's standard variable rate (SVR) you typically fall onto after the introductory period into account.

This can be useful when comparing different mortgage deals, but doesn't consider that many people remortgage onto another deal before they move onto the SVR.

| LTV | Best 2 year fixed mortgage rates |

|---|---|

| 90% | Halifax Initial rate: 4.65% | APRC: 7% Repayment mortgage of £270,000.00 over 25 years, representative APRC 7%. Repayments: 26 months of £1,522.32 at 4.65% (fixed), then 274 months of £1,918.12 at 7.24% (variable). Total amount payable £565,145.20. Early repayment charges apply until 30-Sep-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1099. |

| 80% | Halifax Initial rate: 4.49% | APRC: 7% Repayment mortgage of £240,000.00 over 25 years, representative APRC 7%. Repayments: 26 months of £1,331.33 at 4.49% (fixed), then 274 months of £1,703.07 at 7.24% (variable). Total amount payable £501,255.76. Early repayment charges apply until 30-Sep-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1099. |

| 70% | Bank Of Ireland Initial rate: 4.45% | APRC: 6.8% Repayment mortgage of £210,000.00 over 25 years, representative APRC 6.8%. Repayments: 27 months of £1,161.30 at 4.45% (fixed), then 273 months of £1,452.73 at 6.94% (variable). Total amount payable £427,950.39. Early repayment charges apply until 31-Oct-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1705. Legal fees £258. |

| 60% | Halifax Initial rate: 4.33% | APRC: 6.9% Repayment mortgage of £180,000.00 over 25 years, representative APRC 6.9%. Repayments: 26 months of £982.26 at 4.33% (fixed), then 274 months of £1,275.83 at 7.24% (variable). Total amount payable £375,116.18. Early repayment charges apply until 30-Sep-2028. Arrangement, mortgage discharge, valuation and CHAPS fees total £1099. |

The above fixed rates are provided by Mojo Mortgages and updated every 12 hours. THEY MAY NOT BE AVAILABLE WHEN YOU'RE READY TO SUBMIT AN APPLICATION.

Take a look at the current average mortgage rates in the UK. You can also see the average two-year fixed-mortgage rate over the past year below.

Average rates are provided by Mojo Mortgages and based on their analysis of deals available from five of the biggest lenders at the time

What is a 2 year fixed-rate mortgage?

With a two-year fixed-rate mortgage, your interest rate stays the same for the first two years of your deal. So your mortgage repayments won't rise, no matter what happens to interest rates during that time.

Like the majority of mortgage deals, most two-year fixed-rate mortgages charge fees if you leave or repay the mortgage balance before the end of the deal term.

Once the two years have passed, you should be able to switch to a new fixed or variable-rate deal without penalty.

Should I get a 2 year fixed rate mortgage?

A 2-year fixed-rate mortgage deal is a home loan with an interest rate that stays the same for two years. It’s typically the shortest fixed-term mortgage available, and means your monthly repayments remain the same for 24 months.

As it protects against any market fluctuations, it’s ideal for those who want to know what their outgoings will be, as it makes budgeting easier. It’s also a good option if you aren’t ready to lock into a longer-term deal, or if interest rates are expected to rise in the future.

While two year fixes have historically been cheaper than five year fixed-rate mortgages, this is not always the case. As such, it’s a good idea to compare 2 year fixed rate mortgages before you decide.

“Once you’ve found a rate you’re happy with, move quickly in order to secure it. In some cases lenders are only providing a couple of hours’ notice before increasing rates, so have your documents ready and get them to your broker as soon as possible.”

Laura Hamilton, Mortgage Expert

Advantages of a 2 year fixed-rate mortgage

Your repayments won't rise for two years, even if mortgage rates go up

Knowing how much you’ll be paying each month makes it easier to manage your finances

If interest rates rise across the market, you're likely to be paying less than on a variable-rate deal

If rates fall or you want to move house, you only have to wait two years at most to pay off your mortgage without facing ERCs

Disadvantages of a 2 year fixed-rate mortgage

You’ll generally pay higher mortgage rates than variable rate deals at the start

You’ll lose out on more competitive rates if interest rates fall during your two year fixed rate mortgage term

You’ll usually pay a higher arrangement fee for a fixed-rate

You’ll need a new deal in two years, which means more remortgage fees

If you want to switch your mortgage within two years, you’ll usually still have to pay ERCs to leave early

What happens when my 2 year fixed rate mortgage ends?

When your two year fixed rate period ends, you automatically move on to your lender’s standard variable rate (SVR). This is almost always higher than mortgage deals available from your existing and new lenders.

To avoid the SVR, it's best to start looking at your remortgage options six months before your deal comes to an end. This allows you to lock in a rate early that may not be available in six months time. You then transfer to the new deal when your rate ends, instead of the SVR. This includes 5 year fixed rate and 10 year fixed rate mortgage deals.

The best thing is, if you see a better mortgage rate in the meantime, you can still switch, as you're not locked into a new deal until your existing one expires.

Can I fix my mortgage for longer?

Yes, fixed-rate mortgage deals are available for two, three, five, seven and 10 years - with some lenders offering them for even longer.

Longer deals can help you maintain long-term financial stability and may be a good option if you expect mortgage interest rates to rise.

However, it’s worth weighing this up against the fact that you'd likely have to pay a considerable amount in early repayment charges (ERCs) to leave a longer deal early if rates do fall.

It's difficult to see ahead and predict what mortgage rates may be doing in five or ten years, but keeping up with mortgage news regularly can be helpful.

2 year fixed-rate mortgage deals offer peace of mind that your rate will remain the same for two years. Remember to lock in competitive rates quickly in the current market – a broker can help you to avoid missing out.”Laura Hamilton, Mortgage Expert

Customer Reviews

Highly recommend if you want a pain free mortgage experience

Fantastic experience with Jo Kelly…

Kyle as always was very helpful and…

2 year fixed rate mortgages FAQs

Do you need a larger deposit to get a two-year fixed-rate mortgage?

No, the length of deal has no impact on your deposit size. Some two-year fixed-rate mortgages can be taken out with a very small deposit, such as 5% of the property’s value.

However, the bigger your deposit, the better the mortgage interest rates you’ll be offered by lenders. The best mortgage rates are usually available for buyers with a deposit worth at least 40% of the purchase price.

How much can I borrow on a two-year fixed-rate mortgage?

How much you can borrow will depend on your circumstances. Lenders have specific criteria, no matter what type or length of mortgage deal you opt for. Factors that impact how much you can borrow include:

How much you earn – most lenders will offer around four and a half times your income, but it can be more for higher earners and those in certain professions

How much you can put down as a deposit – the more you put down, the more you can typically borrow

How much you already owe – on things like other loans and credit cards

How much you spend – for example on household bills or child maintenance

What fees are involved in two-year fixed-rate mortgages?

Taking out any mortgage involves paying various fees. These can include:

Arrangement fees, which can range from £0 to more than £2,000

Legal fees, which vary depending on the property type and size

Deposit

Stamp duty

When searching for the best two-year fixed-rate mortgage, it’s therefore important to consider the total cost including fees, not just the mortgage rate on offer. The best way to do this is by looking at the total cost over the initial deal period.

Can you leave a 2 year fixed rate mortgage term early?

You’ll have to pay ERCs (early repayment charges) if you want to pay the mortgage off early. These can be up to 5% of the total amount still owed on your mortgage.

If you’re within the last six months of your two-year fix, it’s possible to lock in a new mortgage deal that you'll automatically transfer onto without having to pay ERCs, once your deal ends.

How do I choose the best 2 year fixed rate mortgage?

The 'best 2 year fixed rate' depends on the individual, as what is best for some might not be best for all. Remember the lowest 2 year fixed rate mortgage won't necessarily be deemed 'best' by all if it has restrictive terms that aren't suitable to the borrower.

Equally, not all borrowers will have access to the cheapest deals, depending on their personal and financial circumstances, as well as the type of property they are mortgaging or remortgaging, and how it meets the criteria of the specific lender offering that rate.

Overall, it's a good idea to seek help from a mortgage broker to secure the best 2 year fixed rate deal for your individual needs.

Can I pay off a 2-year fixed-rate mortgage before it ends?

Yes, if you have the cash to be able to do so. Keep in mind that you may be subject to early repayment charges.

Can I port my two-year fix if I move home?

If you’re going to move house before your fixed-term mortgage ends, mortgage porting allows you to transfer your current deal over to a new property. It can be useful for saving on fees and taking out a new mortgage. Keep in mind that not every mortgage can be ported, and it’ll need to be reassessed by your lender ahead of time.

Are two-year fixed-rate mortgages more expensive than five-year mortgages?

Although two-year fixed mortgage rates are usually lower than five-year rates, market volatility can shift this. It’s worth comparing the latest mortgage rates and working with a mortgage broker if you’re in the market for a new deal.

Didn’t find what you were looking for?

Read some of our most popular guides

About the author

We’ve been featured in

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions.

Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website.

Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH.

Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215)

Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH. To contact Mojo by phone, please call 0333 123 0012.