- Uswitch.com>

- Mortgages>

- Best 3 Year Fixed Rate Mortgages

Compare 3 year fixed rate mortgages

Tell us about yourself and use an expert comparison call with our broker partner Mojo to find your best 3-year fixed-rate mortgage deal from the latest rates in April 2026

How we operate

Our content is regularly reviewed by a team of our expert writers and our services are provided at no cost to you. Learn more about partnership content and how we make our money.

Here’s how to compare 3 year fixed rate mortgages with us

Tell us your mortgage needs

Get a recommendation from across 1000s of 2 year fixed rate mortgage deals

Secure more than just a 2 year fixed rate mortgage offer

Compare 3 year fixed rate mortgages from over 60 lenders across the whole of the market

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

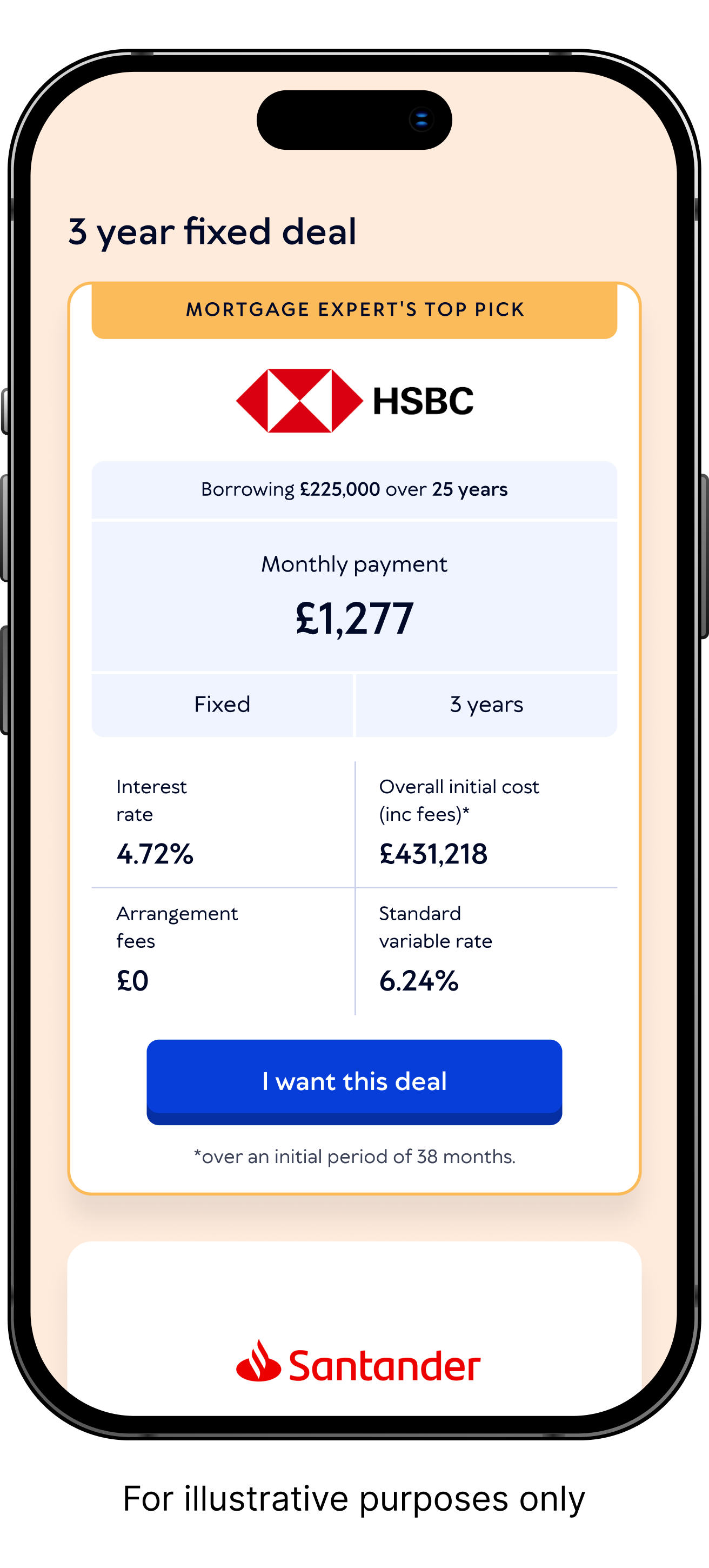

What is a 3 year fixed-rate mortgage?

A 3 year fixed-rate mortgage is a home loan where your interest rate stays the same for the first three years in your deal. Your monthly repayments don’t change, no matter what happens to the interest rates in that time – making it much easier to budget.

While 2- and 5-year fixed rate mortgage deals tend to be the norm, some lenders offer 3-year fixed rate mortgage deals, giving you more options to lock in a rate you’re comfortable with for a little longer than two years, without having to commit to five or 10 years.

Once the 3 years have passed, you could switch to a new fixed or variable-rate deal.

Advantages of a 3-year fixed-rate mortgage

Your monthly repayments won’t change for three years, even if mortgage rates rise. You’ll know what to expect each month, making budgeting easier.

If interest rates rise during your fixed term, your payments won’t be affected, meaning you save money compared to a variable-rate mortgage.

A 3-year fix is a good balance, locking in peace of mind for longer than two years, but it’s not as much of a commitment as a five-year term.

Disadvantages of a 3-year fixed-rate mortgage

If interest rates fall, you won’t benefit from lower repayment costs in the way you would with variable-rate deals, such as tracker and discount mortgages would.

You may pay a slightly higher rate at the start of the term, compared to shorter-term fixes.

If you have plans to move house or switch deals, you may face early repayment charges (ERCs) to change mortgages.

What happens when my 3-year fixed-rate mortgage ends?

Once your 3-year fixed-rate mortgage ends, you’ll typically be moved to your lender's standard variable rate (SVR), which is usually more expensive.

To avoid a spike in your monthly payments, it’s a good idea to start shopping for remortgage deals about six months ahead of your deal ending. Securing a new rate early protects you from potential price hikes, yet doesn't prevent you from switching to a better offer if rates drop before your current deal officially expires.

Can I fix my mortgage for longer?

Yes, fixed-rate mortgage deals are available for 2, 3, 5, and 10 years - with some lenders offering them for even longer.

Longer deals can help you maintain long-term financial stability and may be a good option if you expect mortgage interest rates to rise.

However, it’s worth weighing this up against the fact that you'd likely have to pay a considerable amount in early repayment charges (ERCs) to leave a longer deal early if rates do fall.

It's difficult to see ahead and predict what mortgage rates may be doing in five or ten years, but keeping up with mortgage news regularly can be helpful.

Customer Reviews

Made easy by MOJO

Really simple process

Very good service for both mortgages…

3 year fixed rate mortgages FAQs

Is it a good time to get a 3 year fixed rated mortgage in 2026?

A three-year fixed mortgage is becoming a popular option among borrowers, as it gives a good chunk of time for you to budget and keep your monthly repayments the same. It offers more stability than a 2-year fix, and it gives you the opportunity to switch to a new deal before five years is up.

It’s difficult to predict what interest rates will do – lower or increase. Whether getting your best 3 year fixed rate mortgage is a good idea will depend on your individual circumstances and situation. A good mortgage broker will be able to help, if you’d like.

Can I pay off a three year fixed rate mortgage before it ends?

Yes, you can, though you may be subject to early repayment charges.

How to choose the best 3-year fixed rate mortgage?

If you’re thinking about getting a 3-year fixed rate mortgage, it’s a good idea to research ahead of time. You can check out the latest rates above, and get in touch with a mortgage broker, if you’d like.

What are my other mortgage options?

If you think a fixed-rate mortgage will suit your needs, you could choose a shorter 2-year fixed-rate mortgage, or even a longer, five or ten-year fixed deal.

If you’re open to other forms of mortgages, there are variable-rate deals, such as tracker or discount mortgages. With these products, the rates can go up or down, either directly in line with the Bank of England base rate or in response to market changes.

Didn’t find what you were looking for?

Find out about other mortgages

Read some of our most popular guides

About the author

We’ve been featured in

YOUR HOME/PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP WITH YOUR MORTGAGE REPAYMENTS.

The FCA does not regulate mortgages on commercial or investment buy-to-let properties.

Uswitch makes introductions to Mojo Mortgages to provide mortgage solutions.

Uswitch and Mojo Mortgages are part of the same group of companies. Uswitch Limited is authorised and regulated by the Financial Conduct Authority (FCA) under firm reference number 312850. You can check this on the Financial Services Register by visiting the FCA website.

Uswitch Limited is registered in England and Wales (Company No 03612689) The Cooperage, 5 Copper Row, London SE1 2LH.

Mojo Mortgages is a trading style of Life's Great Limited which is registered in England and Wales (06246376). Mojo are authorised and regulated by the Financial Conduct Authority and are on the Financial Services Register (478215)

Mojo’s registered office is The Cooperage, 5 Copper Row, London, SE1 2LH. To contact Mojo by phone, please call 0333 123 0012.